A transfer to Russia can be delayed or returned even when the payment itself is lawful. The usual causes are incomplete recipient details, a restricted bank or intermediary, an unclear payment purpose, extra compliance review, or a route that no longer supports Russia. Do not resend immediately: first identify where the payment stopped and what evidence the bank needs.

Need a route check before you try again? NoWALL can review the sender country, recipient bank, currency, amount and payment purpose before a new transfer is arranged. This reduces avoidable errors, but it cannot guarantee bank acceptance or remove sanctions and compliance checks. Ask NoWALL about your payment.

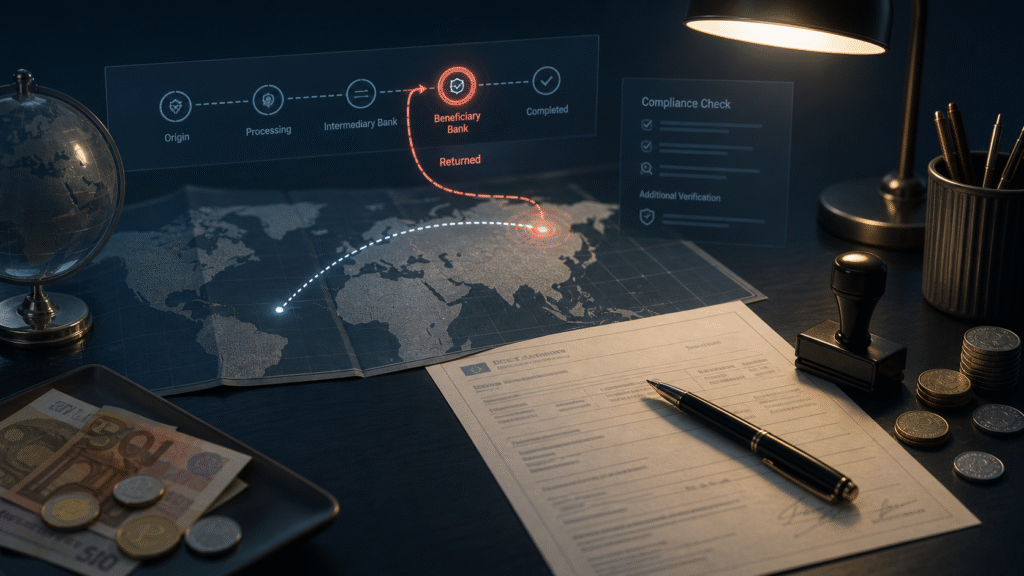

What “delayed”, “rejected” and “returned” actually mean

These status words describe different stages. A delayed payment is still being processed or reviewed. A rejected payment was not accepted into the route, often before funds left the sending institution. A returned payment moved further, then came back after an intermediary or recipient bank declined it.

| Status | What may be happening | Best next step |

|---|---|---|

| Pending or delayed | A bank is checking the sender, recipient, payment purpose or supporting documents. | Ask which institution holds the payment and whether a response deadline applies. |

| Rejected | The provider, sender bank or route does not support the transaction. | Request the exact rejection reason before trying another method. |

| Returned | An intermediary or recipient bank sent the funds back. | Obtain the return message, fee breakdown and final credited amount. |

| Recipient cannot see funds | The payment may be posted under review, credited to a different account, or waiting for recipient action. | Have the recipient contact their bank with the reference number. |

A bank transfer is a chain, not a single handoff. The sender bank may use one or more correspondent banks before the recipient bank receives the instruction. Any institution in that chain may pause the payment to check names, ownership, geography, currency or the economic reason for the transfer.

Seven common reasons a transfer to Russia is delayed or returned

1. The recipient details do not match the bank record

A misspelled name, outdated account number, incorrect bank identifier or missing patronymic can trigger manual review. Card numbers and bank account details are not interchangeable. For a business recipient, the legal name and registration details should match the invoice and the receiving account.

2. A bank in the payment chain is restricted

The recipient bank may be able to receive domestic payments but not the chosen international currency. A correspondent bank may also refuse Russia-related traffic under its own risk policy. Official sanctions lists and banking restrictions change, so a route that worked before may not remain available.

For US-linked payments, the US Treasury’s OFAC FAQ 1202 explains that personal, non-commercial remittances are generally not the target of US Russia sanctions, while transactions involving blocked persons or otherwise prohibited activity remain restricted. That distinction does not require a bank to process every eligible payment.

3. The payment purpose is vague or inconsistent

Descriptions such as “help”, “services” or “invoice” may not give a bank enough context. The payment purpose should truthfully describe the transaction and agree with the supporting document. A personal family transfer should not look like payment for commercial work; a supplier payment should match the contract and invoice.

4. The provider does not support Russia

A familiar brand may accept the initial form but later cancel the transaction when the destination or recipient is checked. Wise lists Russia among unsupported locations and says transfers to or from unsupported countries can be cancelled or refunded; see its current country availability guidance. Western Union has also suspended operations in Russia, as explained in our guide to Western Union and Russia.

5. The bank needs more evidence

Compliance teams may request proof of source of funds, the relationship between sender and recipient, an invoice, a contract, tax information or an explanation of the payment. A request for documents is not automatically a refusal. Delays often grow when the response is incomplete or the documents contradict the transfer instruction.

6. Names or ownership create a screening match

A name may resemble one on a sanctions list even when the person is unrelated. Companies can also require ownership checks. Banks may need a date of birth, address, registration number or ownership chart to clear a possible match. Never alter a name or split a payment to avoid screening.

7. Currency conversion or correspondent access fails

The sender may initiate euros or dollars while the receiving arrangement expects rubles or another settlement currency. If no participating bank can complete the conversion and settlement, the payment may be returned. Ask where conversion occurs, which amount the recipient should receive, and which fees can be deducted along the way.

What to do before sending the money again

- Get the exact status. Ask whether the payment is pending, rejected, cancelled or returned.

- Identify the institution holding it. The sender bank should be able to say whether funds are still internal, with a correspondent, or at the beneficiary bank.

- Request the payment reference and return reason. For a bank transfer, ask for the trace or message reference and any reason code or narrative.

- Confirm the recipient details directly. Recheck the legal name, account, bank name, bank code and supported receipt currency.

- Prepare the evidence. Match the transfer purpose to the real transaction and supporting documents.

- Review the route before resending. Confirm that every known institution can handle the sender country, recipient bank, currency and payment type.

Do not send a duplicate while the first transfer is still pending. Two simultaneous payments can create a larger problem, especially if the original is later released.

Details and documents to have ready

- Sender’s full legal name, address and identity document if requested

- Recipient’s full name exactly as held by the bank

- Recipient account number and the bank’s full name and identifiers

- Expected receipt currency and whether conversion is required

- Truthful payment purpose in plain language

- Evidence of the relationship for a personal transfer, when requested

- Contract, invoice, acceptance document or service description for a commercial payment

- Source-of-funds evidence, such as a bank statement or payslip, when relevant

- Original payment receipt, trace reference and any bank correspondence

For the broader preparation list, use our guide to sending money from Europe to Russia. If your main concern is legality, read the sanctions and bank-check overview before choosing a route.

Compliance checks: what banks are looking for

Banks do more than compare names with lists. They assess the parties, ownership, geography, payment purpose, goods or services involved, currency and the institutions used. They may also apply stricter internal policies than the minimum legal prohibition.

For EU-linked payments, the European Commission maintains a consolidated Russia sanctions FAQ. Its March 2026 guidance on payment services also stresses reasonable steps to identify and mitigate circumvention risks. Using an intermediary does not make a prohibited payment acceptable.

Never disguise the recipient, payment purpose or ownership, and do not divide one payment into smaller amounts to avoid review. If a payment may involve a listed person, controlled company, restricted service or regulated goods, obtain professional legal advice for the relevant jurisdiction before proceeding.

How long should you wait?

There is no universal timeline. A simple correction can take a business day, while correspondent-bank tracing or enhanced review can take longer. Ask the sending institution for a written status, the next review date and any document deadline. If funds are being returned, ask whether intermediary fees and exchange-rate changes will affect the amount credited back.

A useful escalation includes the transaction date, amount, currency, recipient, reference number, current status and a precise question. “Where is my money?” is understandable, but “Which institution currently holds payment reference X, and what information is outstanding?” is easier for an operations team to answer.

Frequently asked questions

Can a lawful personal transfer still be returned?

Yes. A payment can be lawful yet fall outside a provider’s supported routes or internal risk policy. It can also fail because of inaccurate details, an unavailable correspondent bank or incomplete evidence.

Should I try another provider immediately?

Not until you know whether the first payment is still active and why it failed. A second provider may use the same correspondent bank or reject the same recipient details.

Will I receive the full amount back?

Not always. Intermediary charges, return fees and currency conversion can reduce the final credit. Request an itemised explanation if the returned amount differs from the amount sent.

Can NoWALL guarantee that a transfer will arrive?

No. NoWALL can review the payment scenario and available route, but banks, payment partners and compliance teams make their own decisions.

What is the most useful document when tracing a transfer?

The payment reference or bank message is usually the starting point. Combine it with the transfer receipt, recipient details and all requests for additional information.

Last reviewed: 10 July 2026. Payment routes, provider coverage and sanctions rules can change. Confirm the current position with the institutions involved before sending funds.